Research Topics

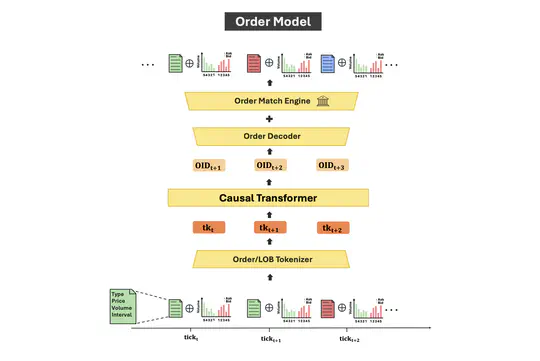

High-frequency financial data — order books, trade events, tick-by-tick prices — poses unique modeling challenges: extreme noise, irregular sampling, heavy-tailed return distributions, and volatility clustering at multiple timescales. Deep learning, and in particular large Transformer-based architectures, has emerged as a powerful approach to capturing the complex temporal dynamics of financial markets at this granularity.

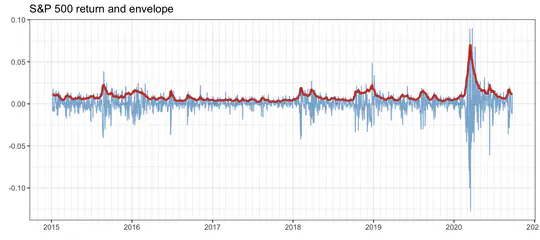

Financial time series — asset returns, volatility, intraday prices — exhibit rich temporal structure that the simple i.i.d. model fails to capture. Econometrics provides the statistical and mathematical framework for modeling returns conditioned on historical observations, with two central families of models: mean models (AR, ARMA, VAR, and state-space models via the Kalman filter) that describe the conditional expected return; and volatility models (GARCH and stochastic volatility) that capture time-varying conditional variance, including the well-documented phenomenon of volatility clustering.

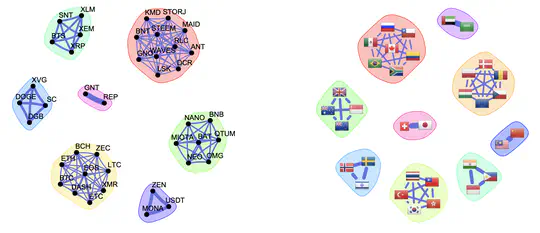

Financial markets generate high-dimensional, non-Gaussian, and time-varying data that challenge classical statistical models. Graph-based representations offer a principled way to capture the dependency structure among assets — stocks, cryptocurrencies, FX rates — and to reveal market sectors, risk propagation channels, and crisis dynamics that are invisible to traditional analysis.

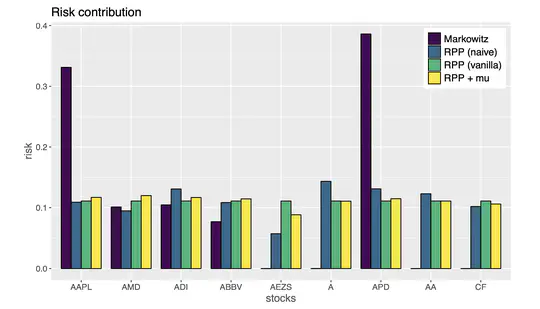

Portfolio optimization — the systematic construction of asset allocations that balance return and risk — is a central problem in quantitative finance. Our research develops rigorous, computationally efficient methods that go well beyond the classical Markowitz mean-variance framework to address the real complexities of financial data.

Past Research Topics

Traditional convex optimization methods and signal processing techniques can be employed in big data problems characterized by large amounts of data in high-dimensional spaces. However, big data brings additional difficulties that need to be taken care of such as high-computational cost that require simple and efficient methods, distributed implementations, faulty data in the form of outliers, etc.

The design of communication systems depends strongly on the degree of knowledge of the channel state information (CSI). The best spectral efficiency and/or performance is obviously achieved when perfect CSI is available at both sides of the link.

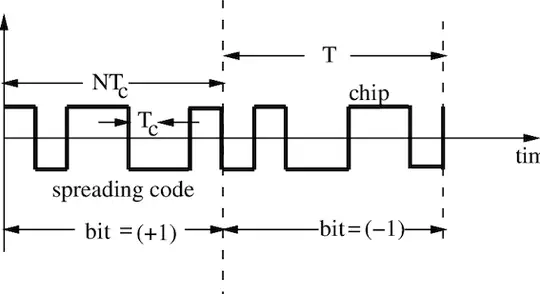

Carefully designed sequences lie at the heart of virtually any digital system commonly used in our daily lives. Examples include GPS synchronization, multiuser CDMA systems, radar ambiguity function shaping, cryptography for secure transactions, and even the watermarking of digital images or videos.

Multiple-input multiple-output (MIMO) channels provide an abstract and unified representation of different physical communication systems, ranging from multi-antenna wireless channels to wireless digital subscriber line systems. They have the key property that several data streams can be simultaneously established.

Semidefinite programming (SDP) is a class of convex optimization problems with a rich theory that can be efficiently solved in polynomial time. Many problems in wireless communications and radar systems can be formulated as SDPs with additional rank constraints.

The Variation Inequality (VI) problem constitutes a very general class of problems in nonlinear analysis. The VI framework embraces many different types of problems such as systems of equations, optimization problems, equilibrium programming, complementary problems, saddle-point problems, Nash equilibrium problems, and generalized Nash equilibrium problems.

Radio regulatory bodies are recently recognizing that rigid spectrum assignment granting exclusive use to licensed services is highly inefficient. A more efficient way to utilize the scarce spectrum resources is with a dynamic spectrum access, depending on the real spectrum usage and traffic demands.

Information theory and estimation theory have generally been regarded as two separate theories with little overlap. Recently, however, it has been recognized that the relations between the two theories are fundamental (e.

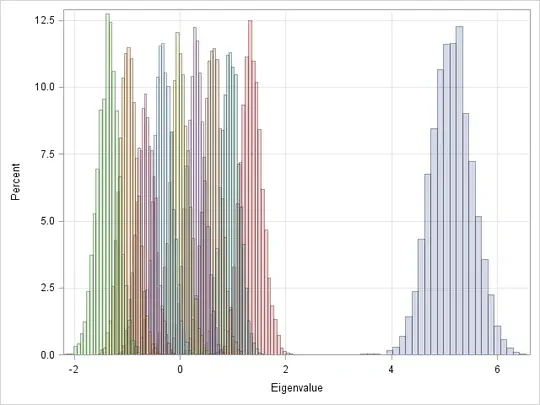

The performance of multiple-input multiple-output (MIMO) communication systems is related to the eigenstructure of the channel matrix H (channel eigenmodes) or, more exactly, to the non-zero eigenvalues of HH†. Therefore, the probabilistic characterization of these eigenvalues is necessary in order to derive analytical expressions for the average and outage performance measures of the system.

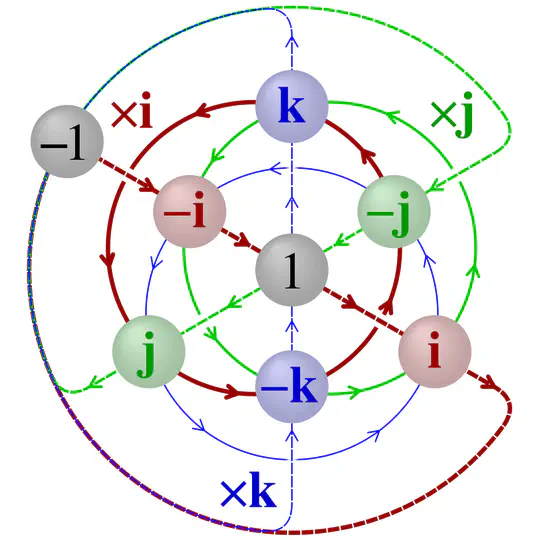

The use of complex numbers allows for a compact notation in many areas such as in baseband representation of communication systems. Quaternions constitute a further step: they are four-dimensional hypercomplex numbers.

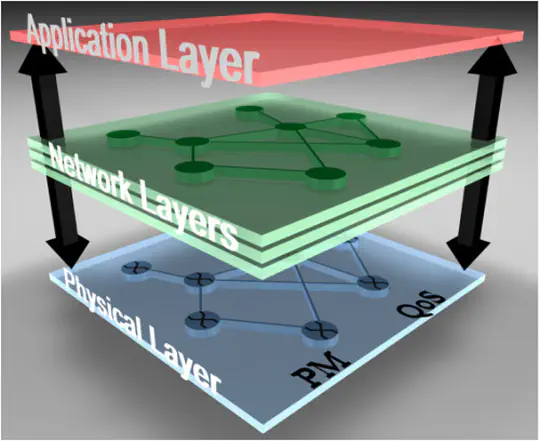

During the last decade, it has been widely recognized that an independent optimization of the different OSI layers in a communication system is a limiting design factor. Instead, a cross-layer design is necessary.

Many communication systems of interest contain multiple uncoordinated users that share a common medium (e.g., wireless ad-hoc networks). These systems can be mathematically modeled as the so-called interference channel, for which the capacity region is still unknown.

Beamforming in wireless communication systems with multiple receive antennas has been studied for the last three decades. Traditionally, the design of the beamformer is based on either the knowledge of the spatial signature of the signal of interest or the availability of a training sequence.